2025 年美國宏觀經濟對加密貨幣的影響 - Moon or Doom?

Abstract: This research paper examines the current macroeconomic landscape in the United States as of August 2025, characterized by re-accelerating inflation, shifting expectations for Federal Reserve rate cuts, and political pressures from President Donald Trump. Drawing from recent economic data and policy developments, the analysis highlights potential risks such as the scenario of an upcoming financial crisis and its impact on Crypto.

For the cryptocurrency community, these dynamics are particularly relevant: rate cuts enhance liquidity and propelled Bitcoin & other coins higher. While inflation may reinforce Bitcoins role as a potential hedge against currency debasement. Trump's pro-crypto policies, including executive orders supporting digital assets, could further catalyze regulatory clarity and institutional adoption, positioning crypto as a beneficiary in this volatile environment.

My work aims to cut the noise and clear up misconceptions surrounding recession fears by delivering a clear, structured framework for understanding economic downturns (even for newcomers), fostering a reliable environment for informed discussion grounded in raw data.

The U.S. economy is the centerpiece of the global crypto art gallery, its influence changing every digital masterpiece. For simplicity, we’ll focus on this dominant artwork. While countless other works hang on the gallery’s walls, we’ll analyze the most important pieces, those that hold up the gallery and impact us all.

Table of Contents

Preface

What is a recession?

What lead to a recession in the past?

Overview of the current macro economic Situation

Bitcoin, the creation of a post crisis economy

Implications for the Crypto space

Conclusion

Preface

The global economy in 2025 is navigating uncharted waters, with the US experiencing robust equity gains alongside vulnerabilities like inflation and fiscal deficits. For the cryptocurrency community, these conditions are pivotal: monetary policy shifts can amplify liquidity, driving crypto prices, while inflation reinforces digital assets as hedges against the depreciation of fiat currencies. This paper blends scientific analysis with clear & easy-to-understand explanations to cut the noise for the average user. Drawing from macro economic data, political figures like President Trump pro-crypto policies, and much more, we explore how Bitcoin and other digital assets could thrive in a post-crisis economy.

By integrating infamous financial algorithms, we aim to provide actionable insights, particularly for crypto enthusiasts seeking to understand macro impacts.

What is a Recession?

To get everyone on board, we'll clear up any possible knowledge gap.

A recession is a significant decline in economic activity across multiple sectors, typically lasting several months. The National Bureau of Economic Research (NBER) defines it by a sustained drop in real GDP, employment, industrial production, and retail sales. Commonly, two consecutive quarters of negative GDP growth signal a recession, though NBER’s criteria are broader, incorporating qualitative factors like economic sentiment.

Recessions disrupt labor markets, reduce consumer spending, and depress asset prices, often triggered by imbalances such as excessive debt, asset bubbles, or external shocks (e.g., oil crises). For crypto, recessions are double-edged: they can spur sell-offs as investors seek liquidity, but also drive interest in decentralized assets as trust in fiat systems wanes. Understanding this context is crucial for assessing 2025’s risks and crypto’s role.

Need an example?

Several significant economic crises have marked recent decades, notably in 2001, 2008, and 2020.

The 2001 crisis, known as the dot-com bubble, stemmed from speculative investments in internet-based companies, leading to a sharp market correction when many of these firms collapsed.

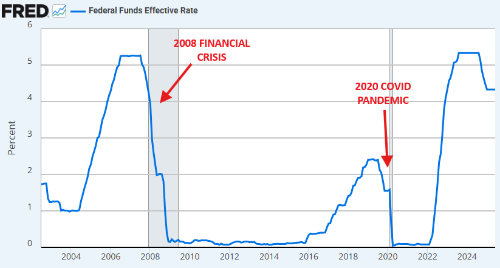

In 2008, the global financial crisis, triggered by a housing market bubble, saw widespread defaults on subprime mortgages and the failure of complex financial instruments like mortgage-backed securities, resulting in severe economic fallout.

The 2020 crisis, unique in its nature, was driven by the COVID-19 pandemic, which caused unprecedented disruptions to global economies through lockdowns, supply chain breakdowns, and market volatility.

What Led to Recessions in the Past? (simplified)

Historically, recessions stem from diverse triggers, often amplified by structural weaknesses:

1973-1975 Oil Crisis Recession: OPEC’s oil embargo quadrupled prices, spiking inflation and stifling growth. US GDP contracted 0.5% in 1974, with unemployment peaking at 9%.

1981-1982 Volcker Recession: The Fed’s aggressive rate hikes to curb double-digit inflation (13.5% in 1980) led to a 2.7% GDP drop and 10.8% unemployment.

2000 Dot-Com Bubble: Overvaluation in tech stocks, with the Nasdaq falling 78% from its peak, triggered a mild recession with 0.3% GDP contraction in 2001.

2008 Financial Crisis: Subprime mortgage defaults and leverage in financial institutions caused a 4.3% GDP decline (2008-2009), with unemployment hitting 10%.

2020 COVID-19 Recession: Lockdowns halted economic activity, shrinking GDP 31.2% annualized in Q2 2020, though stimulus fueled a swift rebound.

Common threads across these crises include excessive speculation (dot-com, housing), monetary policy shifts (Volcker’s hikes), or external shocks (, pandemic)

This is a simplified overview.

Overview of the Current Macroeconomic Situation

& crypto context

The US economy in August 2025 presents a complex picture. Below, I synthesize key trends, incorporating data on market concentration, inflation, Federal Reserve policy, Trump’s influence, fiscal pressures, and institutional positioning, with implications for crypto.

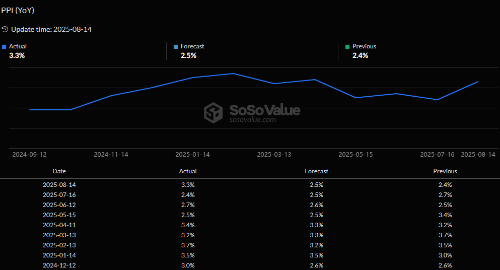

A. Re-Accelerating Inflation

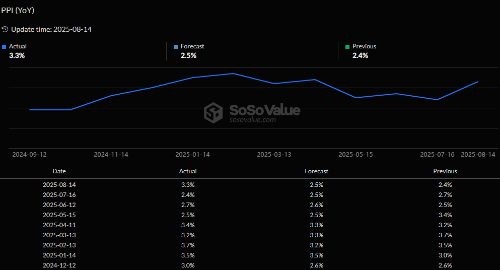

Inflation is rebounding, with core CPI at 3.1% and both headline and core PPI above 3%. Monthly PPI jumped 0.9%, led by 1.1% in services (e.g., 3.8% in machinery wholesaling margins) and 38.9% in vegetables, signaling tariff-induced pressures. Annual PPI hit 3.3%, up from near-zero lows. Tariffs on imports like appliances and clothing are driving costs, challenging the Fed’s 2% target.

*ppi shown not core ppi

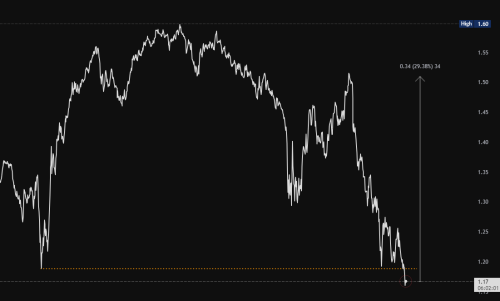

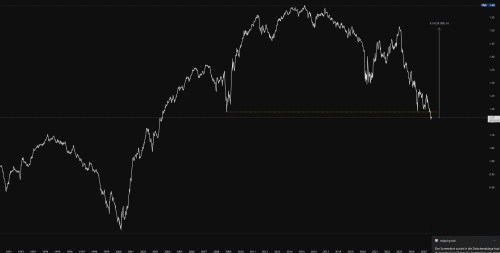

B. Market Concentration in the S&P 500

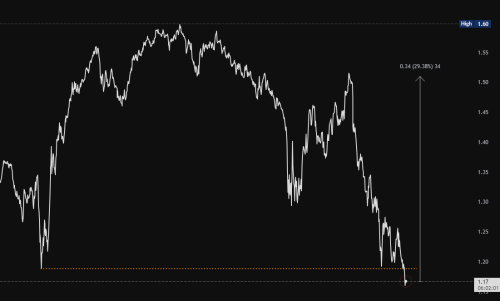

The S&P 500 has surged 34% year-to-date, but the equal-weighted index, where each stock contributes equally, lags. The ratio of the equal-weighted to cap-weighted S&P 500 has fallen to 1.17, its lowest since November 2008, down from 1.51 at the 2022 bear market low.

The “Magnificent 7” tech giants (Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, Tesla) have soared 76%, driving this divergence.

This concentration mirrors Dot-Com Bubble risks, atleast that's a wide spread X opinion. If we zoom out we can see, that we are not near 2001 levels.

Another valuable perspective would be relativity. By looking at the change instead of the raw number, different trends can be seen.

For crypto, a tech stock correction could spill over, as Bitcoin and others often correlate with Nasdaq trends, though their decentralized nature offers diversification.

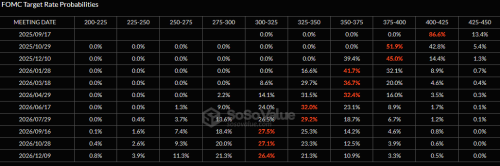

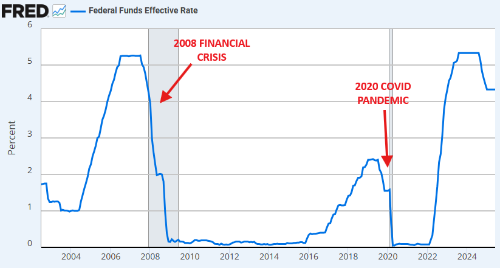

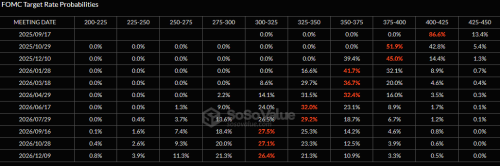

C. Federal Reserve Rate Cut Expectations

Markets now focus on “how many” rate cuts, with a ~87% chance of a September 2025 cut and a base case of three in 2025.

This shift follows softening labor data (unemployment at 4.1%) and growth concerns, despite inflation’s rise. Rate cuts historically boost risk assets, including crypto, by lowering borrowing costs and massively increasing liquidity.

For context. Bitcoin surged 20-50% post-easing in past cycles, and future cut could push it toward $130,000.

By adding global liquidity to he equation with a 12 week lead. We could see a push nearing $150.000.

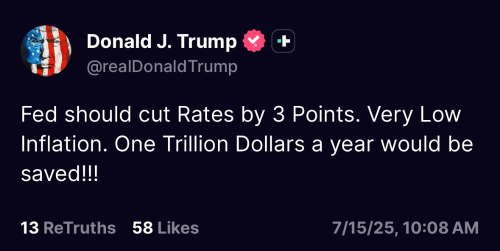

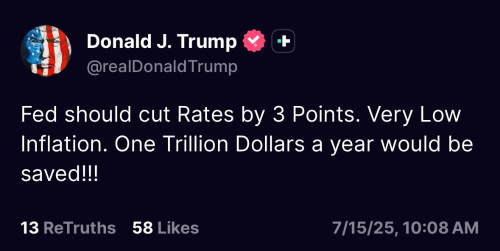

D. President Trump’s Influence

President Trump advocates a 300 basis point rate cut, three times the 2020 emergency cut, to reduce debt interest costs.

$870 billion annually on $29 trillion public debt, though only $174 billion is feasible in year one due to refinancing limits.

He plans to replace Fed Chair Powell, whose term ends May 2026, with a dovish appointee.

The near-term effects on equities would also be explosive. 300 basis points of rate cuts would send the S&P500 above 7,000. But, it would come at a substantial cost, as it wouldn't be far fetched expecting CPI inflation to exceed 5.0% within a year of such drastic rate cuts.

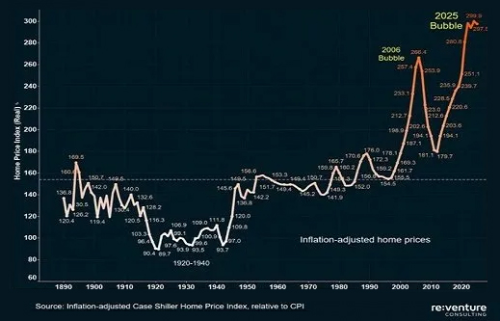

E. Housing, Equities, and Market Impacts

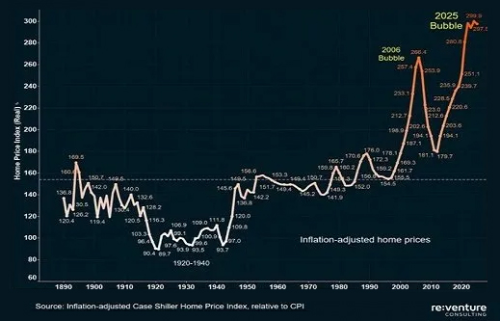

A 300 bps cut could drop mortgage rates to 3%, potentially surging home prices 10%+ in a year, exacerbating affordability.

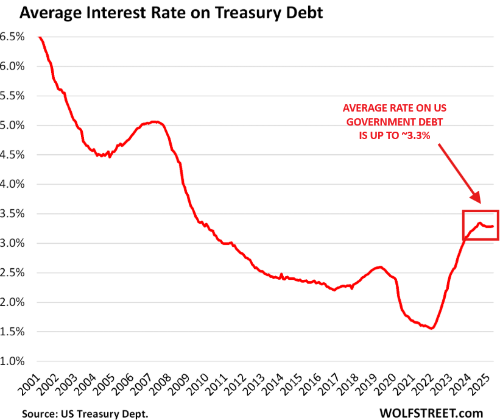

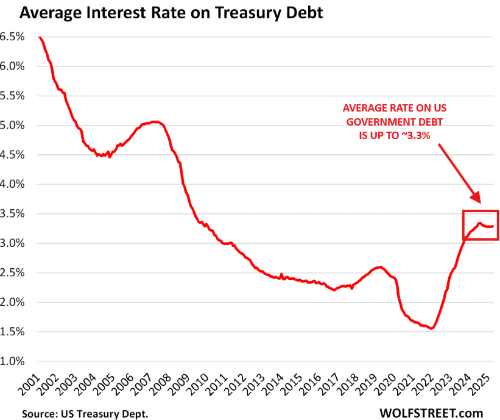

F. US Debt and Budget Deficits

July’s $291 billion deficit, the second-largest for the month, pushes interest expenses above $3 billion daily. Without cuts, costs balloon; with them, inflation risks grow amid trade wars.

G. Institutional Investor Positioning

Institutional equity allocations are at 54.8%, the highest since 2008, 4 points above average, with cash at 17.5% and fixed income at 27.6%.

State Street’s Risk Appetite Index signals euphoria akin to 2000, risking forced sales in downturns. Low cash limits dip-buying, potentially accelerating corrections.

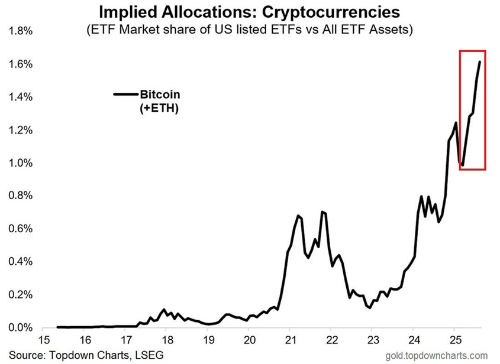

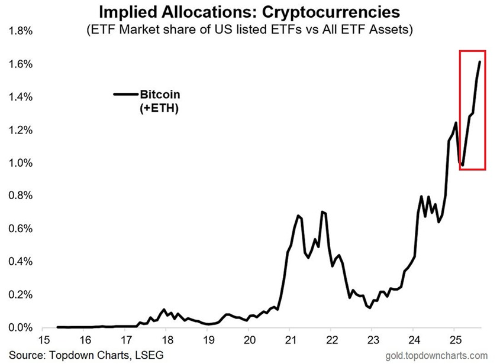

Crypto could see inflows via Bitcoin ETFs, as they are growing rapidly compared to other ETFs ,IF institutions rotate from overcrowded equities.

5. Bitcoin: The Creation of a Post-Crisis Economy

Bitcoin, launched in 2009 post-2008 crisis, was designed as a decentralized currency free from central bank control. In 2025, with deficits soaring and inflation rising, Bitcoin’s fixed supply (21 million coins, halved every four years) positions it as a hedge against currency debasement. Past crises, 2008 and 2020, saw Bitcoin gain traction as trust in institutions faltered.

Trump’s policies amplify this. His executive orders for a Bitcoin strategic reserve and blockchain innovation could integrate crypto into the financial system, reducing regulatory barriers. In a post-crisis economy, where deficits and inflation erode fiat value, Bitcoin offers a store of value, akin to digital gold, with Ethereum and others powering decentralized applications.

6. Implications for the Crypto Space

The 2025 macro environment favors crypto:

Rate Cuts: Three cuts could inject liquidity, lifting Bitcoin and Ethereum 20-50% based on historical cycles. A 300 bps cut, combined with global liquidity trends could push Bitcoin near $150,000

Inflation: Rising CPI and PPI bolster Bitcoin’s hedge appeal, with Ethereum’s deflationary supply adding resilience.

Trump’s Policies: Pro-crypto regulations and a dovish Fed Chair could drive institutional adoption via ETFs and stablecoin frameworks, potentially attracting trillions over the next years.

Risks: Equity corrections, tariff volatility or a full fetched recession will move crypto, though its decentralized nature mitigates risk. To be handled with caution, as crypto never experienced a full fetched Recession.

Personal thesis: A recession in the next few months is not unlikely, navigate with caution and be ready for both scenarios. President Trump and the fed will play a crucial role in this cycle.

7. Conclusion

The US economy in 2025 shall be handled with caution, as intense volatility is seen and can be expected. This will be bring big opportunity in both directions, with market concentration, inflation, and fiscal pressures shaping the volatile landscape.

Historical recessions highlight the dangers of imbalances, yet crypto - led by Bitcoin, offers a resilient alternative. For the crypto community, this is a pivotal moment: rate cuts and inflation favor price appreciation, and regulatory tailwinds promise integration. Investors should monitor Fed and political developments, and leverage crypto’s unique attributes to navigate these historic times.

Picks2025 年美國宏觀經濟對加密貨幣的影響 - Moon or Doom?

Abstract: This research paper examines the current macroeconomic landscape in the United States as of August 2025, characterized by re-accelerating inflation, shifting expectations for Federal Reserve rate cuts, and political pressures from President Donald Trump. Drawing from recent economic data and policy developments, the analysis highlights potential risks such as the scenario of an upcoming financial crisis and its impact on Crypto.

For the cryptocurrency community, these dynamics are particularly relevant: rate cuts enhance liquidity and propelled Bitcoin & other coins higher. While inflation may reinforce Bitcoins role as a potential hedge against currency debasement. Trump's pro-crypto policies, including executive orders supporting digital assets, could further catalyze regulatory clarity and institutional adoption, positioning crypto as a beneficiary in this volatile environment.

My work aims to cut the noise and clear up misconceptions surrounding recession fears by delivering a clear, structured framework for understanding economic downturns (even for newcomers), fostering a reliable environment for informed discussion grounded in raw data.

The U.S. economy is the centerpiece of the global crypto art gallery, its influence changing every digital masterpiece. For simplicity, we’ll focus on this dominant artwork. While countless other works hang on the gallery’s walls, we’ll analyze the most important pieces, those that hold up the gallery and impact us all.

Table of Contents

Preface

What is a recession?

What lead to a recession in the past?

Overview of the current macro economic Situation

Bitcoin, the creation of a post crisis economy

Implications for the Crypto space

Conclusion

Preface

The global economy in 2025 is navigating uncharted waters, with the US experiencing robust equity gains alongside vulnerabilities like inflation and fiscal deficits. For the cryptocurrency community, these conditions are pivotal: monetary policy shifts can amplify liquidity, driving crypto prices, while inflation reinforces digital assets as hedges against the depreciation of fiat currencies. This paper blends scientific analysis with clear & easy-to-understand explanations to cut the noise for the average user. Drawing from macro economic data, political figures like President Trump pro-crypto policies, and much more, we explore how Bitcoin and other digital assets could thrive in a post-crisis economy.

By integrating infamous financial algorithms, we aim to provide actionable insights, particularly for crypto enthusiasts seeking to understand macro impacts.

What is a Recession?

To get everyone on board, we'll clear up any possible knowledge gap.

A recession is a significant decline in economic activity across multiple sectors, typically lasting several months. The National Bureau of Economic Research (NBER) defines it by a sustained drop in real GDP, employment, industrial production, and retail sales. Commonly, two consecutive quarters of negative GDP growth signal a recession, though NBER’s criteria are broader, incorporating qualitative factors like economic sentiment.

Recessions disrupt labor markets, reduce consumer spending, and depress asset prices, often triggered by imbalances such as excessive debt, asset bubbles, or external shocks (e.g., oil crises). For crypto, recessions are double-edged: they can spur sell-offs as investors seek liquidity, but also drive interest in decentralized assets as trust in fiat systems wanes. Understanding this context is crucial for assessing 2025’s risks and crypto’s role.

Need an example?

Several significant economic crises have marked recent decades, notably in 2001, 2008, and 2020.

The 2001 crisis, known as the dot-com bubble, stemmed from speculative investments in internet-based companies, leading to a sharp market correction when many of these firms collapsed.

In 2008, the global financial crisis, triggered by a housing market bubble, saw widespread defaults on subprime mortgages and the failure of complex financial instruments like mortgage-backed securities, resulting in severe economic fallout.

The 2020 crisis, unique in its nature, was driven by the COVID-19 pandemic, which caused unprecedented disruptions to global economies through lockdowns, supply chain breakdowns, and market volatility.

What Led to Recessions in the Past? (simplified)

Historically, recessions stem from diverse triggers, often amplified by structural weaknesses:

1973-1975 Oil Crisis Recession: OPEC’s oil embargo quadrupled prices, spiking inflation and stifling growth. US GDP contracted 0.5% in 1974, with unemployment peaking at 9%.

1981-1982 Volcker Recession: The Fed’s aggressive rate hikes to curb double-digit inflation (13.5% in 1980) led to a 2.7% GDP drop and 10.8% unemployment.

2000 Dot-Com Bubble: Overvaluation in tech stocks, with the Nasdaq falling 78% from its peak, triggered a mild recession with 0.3% GDP contraction in 2001.

2008 Financial Crisis: Subprime mortgage defaults and leverage in financial institutions caused a 4.3% GDP decline (2008-2009), with unemployment hitting 10%.

2020 COVID-19 Recession: Lockdowns halted economic activity, shrinking GDP 31.2% annualized in Q2 2020, though stimulus fueled a swift rebound.

Common threads across these crises include excessive speculation (dot-com, housing), monetary policy shifts (Volcker’s hikes), or external shocks (, pandemic)

This is a simplified overview.

Overview of the Current Macroeconomic Situation

& crypto context

The US economy in August 2025 presents a complex picture. Below, I synthesize key trends, incorporating data on market concentration, inflation, Federal Reserve policy, Trump’s influence, fiscal pressures, and institutional positioning, with implications for crypto.

A. Re-Accelerating Inflation

Inflation is rebounding, with core CPI at 3.1% and both headline and core PPI above 3%. Monthly PPI jumped 0.9%, led by 1.1% in services (e.g., 3.8% in machinery wholesaling margins) and 38.9% in vegetables, signaling tariff-induced pressures. Annual PPI hit 3.3%, up from near-zero lows. Tariffs on imports like appliances and clothing are driving costs, challenging the Fed’s 2% target.

*ppi shown not core ppi

B. Market Concentration in the S&P 500

The S&P 500 has surged 34% year-to-date, but the equal-weighted index, where each stock contributes equally, lags. The ratio of the equal-weighted to cap-weighted S&P 500 has fallen to 1.17, its lowest since November 2008, down from 1.51 at the 2022 bear market low.

The “Magnificent 7” tech giants (Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, Tesla) have soared 76%, driving this divergence.

This concentration mirrors Dot-Com Bubble risks, atleast that's a wide spread X opinion. If we zoom out we can see, that we are not near 2001 levels.

Another valuable perspective would be relativity. By looking at the change instead of the raw number, different trends can be seen.

For crypto, a tech stock correction could spill over, as Bitcoin and others often correlate with Nasdaq trends, though their decentralized nature offers diversification.

C. Federal Reserve Rate Cut Expectations

Markets now focus on “how many” rate cuts, with a ~87% chance of a September 2025 cut and a base case of three in 2025.

This shift follows softening labor data (unemployment at 4.1%) and growth concerns, despite inflation’s rise. Rate cuts historically boost risk assets, including crypto, by lowering borrowing costs and massively increasing liquidity.

For context. Bitcoin surged 20-50% post-easing in past cycles, and future cut could push it toward $130,000.

By adding global liquidity to he equation with a 12 week lead. We could see a push nearing $150.000.

D. President Trump’s Influence

President Trump advocates a 300 basis point rate cut, three times the 2020 emergency cut, to reduce debt interest costs.

$870 billion annually on $29 trillion public debt, though only $174 billion is feasible in year one due to refinancing limits.

He plans to replace Fed Chair Powell, whose term ends May 2026, with a dovish appointee.

The near-term effects on equities would also be explosive. 300 basis points of rate cuts would send the S&P500 above 7,000. But, it would come at a substantial cost, as it wouldn't be far fetched expecting CPI inflation to exceed 5.0% within a year of such drastic rate cuts.

E. Housing, Equities, and Market Impacts

A 300 bps cut could drop mortgage rates to 3%, potentially surging home prices 10%+ in a year, exacerbating affordability.

F. US Debt and Budget Deficits

July’s $291 billion deficit, the second-largest for the month, pushes interest expenses above $3 billion daily. Without cuts, costs balloon; with them, inflation risks grow amid trade wars.

G. Institutional Investor Positioning

Institutional equity allocations are at 54.8%, the highest since 2008, 4 points above average, with cash at 17.5% and fixed income at 27.6%.

State Street’s Risk Appetite Index signals euphoria akin to 2000, risking forced sales in downturns. Low cash limits dip-buying, potentially accelerating corrections.

Crypto could see inflows via Bitcoin ETFs, as they are growing rapidly compared to other ETFs ,IF institutions rotate from overcrowded equities.

5. Bitcoin: The Creation of a Post-Crisis Economy

Bitcoin, launched in 2009 post-2008 crisis, was designed as a decentralized currency free from central bank control. In 2025, with deficits soaring and inflation rising, Bitcoin’s fixed supply (21 million coins, halved every four years) positions it as a hedge against currency debasement. Past crises, 2008 and 2020, saw Bitcoin gain traction as trust in institutions faltered.

Trump’s policies amplify this. His executive orders for a Bitcoin strategic reserve and blockchain innovation could integrate crypto into the financial system, reducing regulatory barriers. In a post-crisis economy, where deficits and inflation erode fiat value, Bitcoin offers a store of value, akin to digital gold, with Ethereum and others powering decentralized applications.

6. Implications for the Crypto Space

The 2025 macro environment favors crypto:

Rate Cuts: Three cuts could inject liquidity, lifting Bitcoin and Ethereum 20-50% based on historical cycles. A 300 bps cut, combined with global liquidity trends could push Bitcoin near $150,000

Inflation: Rising CPI and PPI bolster Bitcoin’s hedge appeal, with Ethereum’s deflationary supply adding resilience.

Trump’s Policies: Pro-crypto regulations and a dovish Fed Chair could drive institutional adoption via ETFs and stablecoin frameworks, potentially attracting trillions over the next years.

Risks: Equity corrections, tariff volatility or a full fetched recession will move crypto, though its decentralized nature mitigates risk. To be handled with caution, as crypto never experienced a full fetched Recession.

Personal thesis: A recession in the next few months is not unlikely, navigate with caution and be ready for both scenarios. President Trump and the fed will play a crucial role in this cycle.

7. Conclusion

The US economy in 2025 shall be handled with caution, as intense volatility is seen and can be expected. This will be bring big opportunity in both directions, with market concentration, inflation, and fiscal pressures shaping the volatile landscape.

Historical recessions highlight the dangers of imbalances, yet crypto - led by Bitcoin, offers a resilient alternative. For the crypto community, this is a pivotal moment: rate cuts and inflation favor price appreciation, and regulatory tailwinds promise integration. Investors should monitor Fed and political developments, and leverage crypto’s unique attributes to navigate these historic times.

00:00

00:00