$HSK – The Compliant Gateway to Asia's Digital Economy

TLDR

HSK, the native token of the HashKey Group, offers a compelling investment opportunity in the regulated crypto market. Despite its current price (~$0.60) reflecting some market anticipation, I believe HSK is significantly undervalued on a long-term basis, presenting a strategic accumulation opportunity. This conviction is driven by HashKey's unparalleled global regulatory licenses (Hong Kong, Singapore, Dubai, Japan, Bermuda, Ireland), its pivotal role in the China/Asia stablecoin ecosystem, and imminent catalysts like major exchange listings. I project a long-term target of $5-$10 per token (9x-17x return), recommending a "buy the dip" strategy for this high-quality asset.

Overview

HashKey Group, backed by the well-capitalized Wanxiang Group, is a leading digital asset financial services platform, strategically positioned as the Asia version of Coinbase. Unlike many exchange-centric tokens (e.g., BGB, MX), HashKey's value proposition extends beyond a singular trading platform. Since its establishment in 2018, HashKey has meticulously built a comprehensive Web3 ecosystem, prioritizing global regulatory compliance across diverse business lines as its core competitive advantage.

Key pillars include:

HashKey Exchange: A globally licensed exchange serving institutions and retail. It holds first-mover advantage with SFC licenses (Type 1 & 7) in Hong Kong, DPT/CMS licenses in Singapore, a VASP license in Dubai (UAE), and licenses/registrations in Japan, Bermuda, and Ireland. This extensive, multi-jurisdictional licensure provides a formidable barrier to entry and a unique value proposition.

Notably, ~45% of HashKey’s trading volume stems from fiat-to-stablecoin conversions, serving as a critical compliant on/off-ramp. This function is central to partnerships with brokers like Futu and ZA Bank, who leverage HashKey’s regulated infrastructure.

HashKey Capital: An influential crypto-native investment firm managing over $1B AUM, with early investments in foundational projects like Ethereum and Circle.

OTC + Payments: Facilitates stablecoin and fiat transactions, serving a diverse client base including hedge funds, family offices, payment processors, and cross-border trading companies. HashKey OTC Global reported a 246% YoY revenue increase in H1 2025. Its highest single-week volume has approached $200 million, demonstrating its capacity for high-value institutional transactions and positioning it as a significant, compliant revenue engine.

HashKey Chain: An Ethereum L2 blockchain (built on OP Stack) designed for compliant RWA and institutional Web3 solutions. This differentiates HashKey significantly by offering its own scalable network for broader ecosystem development.

The HSK token is HashKey Group's native platform token, designed to capture value from this entire diversified group. With a current circulating market cap of ~$150M and an FDV of ~$600M (~25% in circulation), HSK appears undervalued relative to the group's equity valuation and strategic positioning.

Token Value Accrual

HSK's value accrual is directly tied to the overall success of the entire HashKey Group's diverse operations, presenting a more robust model than many exchange tokens (e.g., BGB, MX) which primarily derive value from their associated exchange:

20% Group Revenue Buyback & Burn: The whitepaper commits 20% of HashKey Group's total profits (across all business lines, including exchange, OTC, and chain-related ventures) to HSK buybacks and burns. While not yet active due to the growth phase, this is a significant deflationary mechanism.

Platform Utility & Gas Token: HSK offers benefits like fee discounts. Crucially, HSK is an ERC-20 token on Ethereum L1, which is bridged to serve as the native gas token for HashKey Chain L2. This provides dual utility and demand, not only within the exchange but also as the fundamental fuel for transactions on HashKey's proprietary L2 blockchain. This contrasts with tokens like BGB or MX which primarily function as exchange utility tokens without powering their own dedicated blockchain.

Strategic Binding to a Diversified Ecosystem: HSK's value directly benefits from the comprehensive success of HashKey Capital's investments, robust OTC operations, and any future group ventures, going beyond just exchange trading volume. This broader exposure to multiple revenue streams and strategic plays within Web3 sets HSK apart.

Employee Compensation: HSK is reportedly used for employee compensation (~$0.4 HSK cost), creating vested interest, albeit contributing to short-term selling pressure.

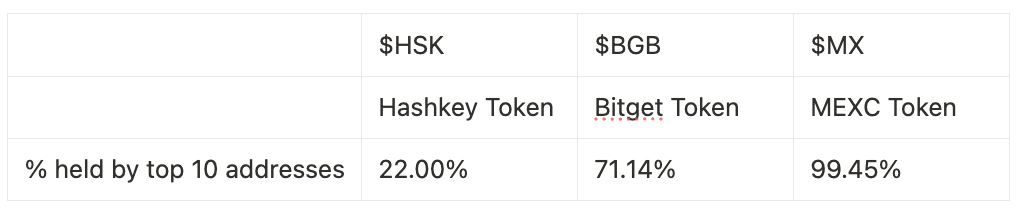

Additionally, HSK demonstrates a significantly healthier token distribution compared to many peer exchange tokens like BGB and MX. A lower percentage of tokens held by the top 10 wallets reduces centralization risks and the potential for market manipulation, fostering a more robust and decentralized ecosystem which enhances long-term investor confidence.

Thesis

My core thesis is that HSK is a deeply undervalued, pure-play investment in compliant crypto infrastructure. The HashKey Group's extensive, multi-jurisdictional license portfolio is its paramount asset, positioning it as the most credible and compliant gateway in Asia's rapidly formalizing crypto landscape. The market is increasingly recognizing that compliant infrastructure is the ultimate competitive moat.

While "coin-stock" valuations are surging (e.g., Coinbase at ~$100B MCAP), HSK, despite its direct involvement in the USDC ecosystem and "Coinbase of the East" ambitions, has yet to fully price in its regulatory leadership. This valuation gap presents a compelling opportunity.

HSK is uniquely poised to benefit from:

Hong Kong's Regulatory Leadership: As the most compliant exchange, it gains disproportionately from Hong Kong's embrace of retail crypto and new stablecoin regulations, attracting capital.

Stablecoin Issuance & Circulation: Its deep ties to the stablecoin ecosystem (e.g., Circle, potential HKD stablecoins) position it for significant revenues from issuance, redemptions, and settlements.

Potential Mainland China Re-engagement: HashKey could serve as a primary conduit if mainland China engages with regulated crypto, including potential clearance of seized assets (~$20B).

The group's strategic focus on its core regulated business, including reportedly divesting non-profitable ventures, further solidifies its value proposition. This, combined with HSK's current low valuation, creates a significant asymmetric risk/reward. I advocate for buying the dips to capitalize on its long-term trajectory.

Why Now?

Despite historical perceptions of slow movement and significant cash burn, I believe HashKey Group is now at a critical inflection point, transitioning forcefully into a monetization and execution phase. This strategic timing is driven by three key factors:

Maturing Regulatory Landscape & HKMA Stablecoins Ordinance: The HKMA Stablecoins Ordinance, effective August 1, 2025, directly benefits HashKey by formalizing fiat-referenced stablecoin issuance. This move firmly positions HashKey as a key player for stablecoin issuance, trading, and institutional settlement within Hong Kong's new regulated framework, significantly enhancing the value of its extensive license portfolio as a scarce asset.

Clearing Internal Overhang & Renewed Market Dynamics: HSK experienced a significant price surge to ~$0.80 in late June, followed by a correction. This volatility, coupled with a notable increase in unique holders (from ~2.7k to ~3.2k, an 18% increase since the surge), suggests a healthy clearing out of previous internal supply overhangs (e.g., from early unlocks or employee compensation). This re-distribution allows for more natural, fundamental-driven price discovery going forward.

Demonstrated Operational Efficiencies & Strategic Volume Pivot: The group is actively addressing historical cost structures. For instance, a recent partnership with Alibaba Cloud (announced May 2025) has reportedly reduced data operation costs by over 50% and significantly improved system stability. While the CEX's direct trading volume was historically less prominent, HashKey's OTC business is now thriving and profitable. As regulatory clarity solidifies further, flows are anticipated to pivot from predominantly OTC rails towards increased retail exchange usage, boosting spot volume over time. This strategic shift emphasizes building an institutional beltway around the on-ramp function, driving broader ecosystem adoption.

Catalyst

Several near-term and medium-term catalysts will drive HSK's re-rating:

Activation of Buyback & Burn: Formal activation of the 20% group revenue buyback and burn will introduce powerful deflationary pressure.

License Value Revaluation & Regulatory Tailwinds: Increasing global regulatory tightening (e.g., Singapore's DPT license tightening) will funnel capital to compliant platforms, driving a significant revaluation of HashKey's license portfolio.

Institutional Adoption & Partnerships: Continued integration with TradFi institutions (Futu, Guotai Junan) will drive transaction volume. The partnerships with Futu and ZA Bank, along with potential JD.com stablecoin integration, will also drive significant new transaction volume and asset diversification beyond just on/off-ramps, leveraging HashKey’s foundational infrastructure.

Stablecoin Ecosystem Growth: HashKey is poised to capitalize on the expansion of stablecoins, particularly a potential HKD stablecoin, increasing its role as a liquidity and settlement layer.

HashKey Chain Adoption: Increased use of its Ethereum L2 will elevate HSK’s utility as a gas token.

Increased User Growth & Hong Kong Inflows: Positive regulatory and market developments could drive a surge in compliant user adoption.

Major Exchange Listings (OKX, Binance): Tier-1 exchange listings would significantly boost liquidity and market awareness. Given OKX's existing presence in Hong Kong, an OKX listing for HSK appears highly probable.

Risks

While compelling, HSK faces notable risks:

Sustainability of Brokerage Partnerships: Long-term reliance of Hong Kong securities firms on HashKey for crypto services and consistent cash flow generation remains uncertain, as these firms may build their own compliance capabilities.

Execution Risk & Operational Challenges: Ambitious vision requires strong execution. Past team changes and the need for improved operational efficiency could hinder growth.

Competition: Despite first-mover advantage, competition from other licensed or even non-compliant exchanges exists.

Profitability & Buyback Timing: Buyback/burn depends on substantial group profitability; delays could impact value accrual.

Low Liquidity & Slippage: Current low trading volume can impact large order execution.

Token Unlocks/Dilution: Monitoring future unlock schedules for the remaining ~75% of supply is crucial, as this could introduce further selling pressure.

Valuation

Direct valuation is complex given HashKey isn't a transparent on-chain protocol or a public company. However, HSK's current ~$150M circulating market cap and ~$600M FDV appear significantly undervalued:

Equity Valuation Discrepancy: Gaorong Ventures' $30M investment at a $1.5B HashKey Group valuation (Feb 2025) implies the group's equity value is more than double the token's FDV. As HSK captures group value, this suggests substantial disconnect and ~100% upside to equity valuation.

Comps: OSL, a smaller HK-licensed exchange, trades at ~$1.4B USD market cap (as a stock), despite roughly 10% of HashKey's transaction volume and less comprehensive ecosystem. This highlights HSK's re-rating potential given its 80% HK market share.

"Coinbase of the East" Narrative: While Coinbase is ~$100B MCAP, even achieving a fraction (e.g., $5B FDV for HSK) represents ~7x increase from current levels, plausible given HashKey's strategic positioning.

Based on fundamental analysis and peer comparisons, a long-term price target for HSK is established between $5 and $10 per token, implying an FDV of $5 billion to $10 billion. This represents a substantial upside potential of ~9x to 17x from the current price. While the token's fair value for short-term accumulation is assessed within the $0.35 - $0.50 range, the present market price of ~$0.60 warrants careful consideration. A "buy the dip" strategy is advocated, accumulating during periods of weakness, as the true value proposition is expected to be unlocked with the explicit activation of the 20% group profit buyback and burn program.

Summary & Outlook

HashKey Group's unique positioning as a globally licensed Web3 ecosystem, extending beyond a singular exchange, offers a compelling investment opportunity in a rapidly formalizing market. While acknowledging past perceptions of operational slowness and primary reliance on on/off-ramps for volume, the analysis strongly indicates a fundamental shift. The HSK token, intrinsically linked to the entire group's diverse and compliant revenue streams, presents significant long-term upside. A strategic "buy the dip" approach is advocated to capitalize on the unlocking of value from its unparalleled regulatory moat, the burgeoning stablecoin ecosystem, and imminent catalysts.

$HSK – The Compliant Gateway to Asia's Digital Economy

TLDR

HSK, the native token of the HashKey Group, offers a compelling investment opportunity in the regulated crypto market. Despite its current price (~$0.60) reflecting some market anticipation, I believe HSK is significantly undervalued on a long-term basis, presenting a strategic accumulation opportunity. This conviction is driven by HashKey's unparalleled global regulatory licenses (Hong Kong, Singapore, Dubai, Japan, Bermuda, Ireland), its pivotal role in the China/Asia stablecoin ecosystem, and imminent catalysts like major exchange listings. I project a long-term target of $5-$10 per token (9x-17x return), recommending a "buy the dip" strategy for this high-quality asset.

Overview

HashKey Group, backed by the well-capitalized Wanxiang Group, is a leading digital asset financial services platform, strategically positioned as the Asia version of Coinbase. Unlike many exchange-centric tokens (e.g., BGB, MX), HashKey's value proposition extends beyond a singular trading platform. Since its establishment in 2018, HashKey has meticulously built a comprehensive Web3 ecosystem, prioritizing global regulatory compliance across diverse business lines as its core competitive advantage.

Key pillars include:

HashKey Exchange: A globally licensed exchange serving institutions and retail. It holds first-mover advantage with SFC licenses (Type 1 & 7) in Hong Kong, DPT/CMS licenses in Singapore, a VASP license in Dubai (UAE), and licenses/registrations in Japan, Bermuda, and Ireland. This extensive, multi-jurisdictional licensure provides a formidable barrier to entry and a unique value proposition.

Notably, ~45% of HashKey’s trading volume stems from fiat-to-stablecoin conversions, serving as a critical compliant on/off-ramp. This function is central to partnerships with brokers like Futu and ZA Bank, who leverage HashKey’s regulated infrastructure.

HashKey Capital: An influential crypto-native investment firm managing over $1B AUM, with early investments in foundational projects like Ethereum and Circle.

OTC + Payments: Facilitates stablecoin and fiat transactions, serving a diverse client base including hedge funds, family offices, payment processors, and cross-border trading companies. HashKey OTC Global reported a 246% YoY revenue increase in H1 2025. Its highest single-week volume has approached $200 million, demonstrating its capacity for high-value institutional transactions and positioning it as a significant, compliant revenue engine.

HashKey Chain: An Ethereum L2 blockchain (built on OP Stack) designed for compliant RWA and institutional Web3 solutions. This differentiates HashKey significantly by offering its own scalable network for broader ecosystem development.

The HSK token is HashKey Group's native platform token, designed to capture value from this entire diversified group. With a current circulating market cap of ~$150M and an FDV of ~$600M (~25% in circulation), HSK appears undervalued relative to the group's equity valuation and strategic positioning.

Token Value Accrual

HSK's value accrual is directly tied to the overall success of the entire HashKey Group's diverse operations, presenting a more robust model than many exchange tokens (e.g., BGB, MX) which primarily derive value from their associated exchange:

20% Group Revenue Buyback & Burn: The whitepaper commits 20% of HashKey Group's total profits (across all business lines, including exchange, OTC, and chain-related ventures) to HSK buybacks and burns. While not yet active due to the growth phase, this is a significant deflationary mechanism.

Platform Utility & Gas Token: HSK offers benefits like fee discounts. Crucially, HSK is an ERC-20 token on Ethereum L1, which is bridged to serve as the native gas token for HashKey Chain L2. This provides dual utility and demand, not only within the exchange but also as the fundamental fuel for transactions on HashKey's proprietary L2 blockchain. This contrasts with tokens like BGB or MX which primarily function as exchange utility tokens without powering their own dedicated blockchain.

Strategic Binding to a Diversified Ecosystem: HSK's value directly benefits from the comprehensive success of HashKey Capital's investments, robust OTC operations, and any future group ventures, going beyond just exchange trading volume. This broader exposure to multiple revenue streams and strategic plays within Web3 sets HSK apart.

Employee Compensation: HSK is reportedly used for employee compensation (~$0.4 HSK cost), creating vested interest, albeit contributing to short-term selling pressure.

Additionally, HSK demonstrates a significantly healthier token distribution compared to many peer exchange tokens like BGB and MX. A lower percentage of tokens held by the top 10 wallets reduces centralization risks and the potential for market manipulation, fostering a more robust and decentralized ecosystem which enhances long-term investor confidence.

Thesis

My core thesis is that HSK is a deeply undervalued, pure-play investment in compliant crypto infrastructure. The HashKey Group's extensive, multi-jurisdictional license portfolio is its paramount asset, positioning it as the most credible and compliant gateway in Asia's rapidly formalizing crypto landscape. The market is increasingly recognizing that compliant infrastructure is the ultimate competitive moat.

While "coin-stock" valuations are surging (e.g., Coinbase at ~$100B MCAP), HSK, despite its direct involvement in the USDC ecosystem and "Coinbase of the East" ambitions, has yet to fully price in its regulatory leadership. This valuation gap presents a compelling opportunity.

HSK is uniquely poised to benefit from:

Hong Kong's Regulatory Leadership: As the most compliant exchange, it gains disproportionately from Hong Kong's embrace of retail crypto and new stablecoin regulations, attracting capital.

Stablecoin Issuance & Circulation: Its deep ties to the stablecoin ecosystem (e.g., Circle, potential HKD stablecoins) position it for significant revenues from issuance, redemptions, and settlements.

Potential Mainland China Re-engagement: HashKey could serve as a primary conduit if mainland China engages with regulated crypto, including potential clearance of seized assets (~$20B).

The group's strategic focus on its core regulated business, including reportedly divesting non-profitable ventures, further solidifies its value proposition. This, combined with HSK's current low valuation, creates a significant asymmetric risk/reward. I advocate for buying the dips to capitalize on its long-term trajectory.

Why Now?

Despite historical perceptions of slow movement and significant cash burn, I believe HashKey Group is now at a critical inflection point, transitioning forcefully into a monetization and execution phase. This strategic timing is driven by three key factors:

Maturing Regulatory Landscape & HKMA Stablecoins Ordinance: The HKMA Stablecoins Ordinance, effective August 1, 2025, directly benefits HashKey by formalizing fiat-referenced stablecoin issuance. This move firmly positions HashKey as a key player for stablecoin issuance, trading, and institutional settlement within Hong Kong's new regulated framework, significantly enhancing the value of its extensive license portfolio as a scarce asset.

Clearing Internal Overhang & Renewed Market Dynamics: HSK experienced a significant price surge to ~$0.80 in late June, followed by a correction. This volatility, coupled with a notable increase in unique holders (from ~2.7k to ~3.2k, an 18% increase since the surge), suggests a healthy clearing out of previous internal supply overhangs (e.g., from early unlocks or employee compensation). This re-distribution allows for more natural, fundamental-driven price discovery going forward.

Demonstrated Operational Efficiencies & Strategic Volume Pivot: The group is actively addressing historical cost structures. For instance, a recent partnership with Alibaba Cloud (announced May 2025) has reportedly reduced data operation costs by over 50% and significantly improved system stability. While the CEX's direct trading volume was historically less prominent, HashKey's OTC business is now thriving and profitable. As regulatory clarity solidifies further, flows are anticipated to pivot from predominantly OTC rails towards increased retail exchange usage, boosting spot volume over time. This strategic shift emphasizes building an institutional beltway around the on-ramp function, driving broader ecosystem adoption.

Catalyst

Several near-term and medium-term catalysts will drive HSK's re-rating:

Activation of Buyback & Burn: Formal activation of the 20% group revenue buyback and burn will introduce powerful deflationary pressure.

License Value Revaluation & Regulatory Tailwinds: Increasing global regulatory tightening (e.g., Singapore's DPT license tightening) will funnel capital to compliant platforms, driving a significant revaluation of HashKey's license portfolio.

Institutional Adoption & Partnerships: Continued integration with TradFi institutions (Futu, Guotai Junan) will drive transaction volume. The partnerships with Futu and ZA Bank, along with potential JD.com stablecoin integration, will also drive significant new transaction volume and asset diversification beyond just on/off-ramps, leveraging HashKey’s foundational infrastructure.

Stablecoin Ecosystem Growth: HashKey is poised to capitalize on the expansion of stablecoins, particularly a potential HKD stablecoin, increasing its role as a liquidity and settlement layer.

HashKey Chain Adoption: Increased use of its Ethereum L2 will elevate HSK’s utility as a gas token.

Increased User Growth & Hong Kong Inflows: Positive regulatory and market developments could drive a surge in compliant user adoption.

Major Exchange Listings (OKX, Binance): Tier-1 exchange listings would significantly boost liquidity and market awareness. Given OKX's existing presence in Hong Kong, an OKX listing for HSK appears highly probable.

Risks

While compelling, HSK faces notable risks:

Sustainability of Brokerage Partnerships: Long-term reliance of Hong Kong securities firms on HashKey for crypto services and consistent cash flow generation remains uncertain, as these firms may build their own compliance capabilities.

Execution Risk & Operational Challenges: Ambitious vision requires strong execution. Past team changes and the need for improved operational efficiency could hinder growth.

Competition: Despite first-mover advantage, competition from other licensed or even non-compliant exchanges exists.

Profitability & Buyback Timing: Buyback/burn depends on substantial group profitability; delays could impact value accrual.

Low Liquidity & Slippage: Current low trading volume can impact large order execution.

Token Unlocks/Dilution: Monitoring future unlock schedules for the remaining ~75% of supply is crucial, as this could introduce further selling pressure.

Valuation

Direct valuation is complex given HashKey isn't a transparent on-chain protocol or a public company. However, HSK's current ~$150M circulating market cap and ~$600M FDV appear significantly undervalued:

Equity Valuation Discrepancy: Gaorong Ventures' $30M investment at a $1.5B HashKey Group valuation (Feb 2025) implies the group's equity value is more than double the token's FDV. As HSK captures group value, this suggests substantial disconnect and ~100% upside to equity valuation.

Comps: OSL, a smaller HK-licensed exchange, trades at ~$1.4B USD market cap (as a stock), despite roughly 10% of HashKey's transaction volume and less comprehensive ecosystem. This highlights HSK's re-rating potential given its 80% HK market share.

"Coinbase of the East" Narrative: While Coinbase is ~$100B MCAP, even achieving a fraction (e.g., $5B FDV for HSK) represents ~7x increase from current levels, plausible given HashKey's strategic positioning.

Based on fundamental analysis and peer comparisons, a long-term price target for HSK is established between $5 and $10 per token, implying an FDV of $5 billion to $10 billion. This represents a substantial upside potential of ~9x to 17x from the current price. While the token's fair value for short-term accumulation is assessed within the $0.35 - $0.50 range, the present market price of ~$0.60 warrants careful consideration. A "buy the dip" strategy is advocated, accumulating during periods of weakness, as the true value proposition is expected to be unlocked with the explicit activation of the 20% group profit buyback and burn program.

Summary & Outlook

HashKey Group's unique positioning as a globally licensed Web3 ecosystem, extending beyond a singular exchange, offers a compelling investment opportunity in a rapidly formalizing market. While acknowledging past perceptions of operational slowness and primary reliance on on/off-ramps for volume, the analysis strongly indicates a fundamental shift. The HSK token, intrinsically linked to the entire group's diverse and compliant revenue streams, presents significant long-term upside. A strategic "buy the dip" approach is advocated to capitalize on the unlocking of value from its unparalleled regulatory moat, the burgeoning stablecoin ecosystem, and imminent catalysts.

00:00

00:00